A policyholder issues an appeal letter for denial of an insurance claim to an insurance company in which they ask for a reevaluation of an earlier decision of the company to deny a benefit. In this letter, the policyholder explains the matter about which a benefit was denied and why they think this should not have been so.

Furthermore, the appeal letter is an effective way to aware the insurance company about the complaint made by the policyholder. After that, the company reviews the earlier decision and decides whether to overturn the decision or reaffirm it.

Table of Contents

What is the purpose of an insurance appeal letter?

The main purpose of an insurance appeal letter is to tell an insurance company of a complaint from a policyholder regarding a denied benefit. This letter is an effective means to convince the insurance company to reconsider by presenting relevant details.

The insurance appeal letter is written after receiving a notification from an insurance company stating that an expense will not be covered under an insurance plan. The policyholder by writing this letter requests money that has already been deposited with the insurance company.

The important components of an appeal letter:

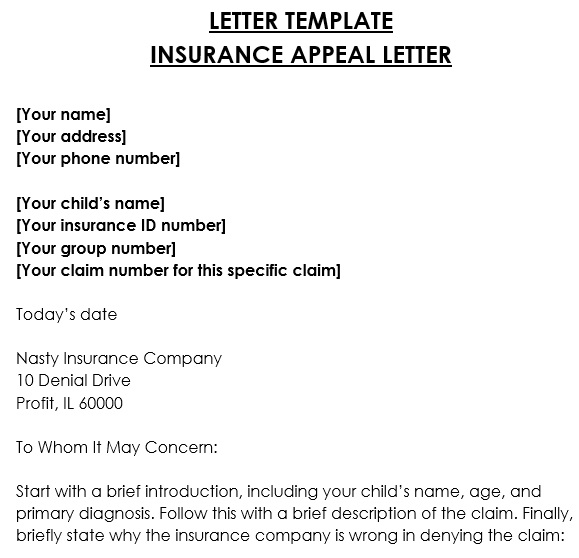

The important components to include in an insurance appeal letter are;

- Current date

- Name and contact details of the sender

- The name and contact details of policyholder as well as policy number

- The purpose of writing the letter

- The situation about which a benefit was denied

- The reason mentioned on the denial notification letter

- The date when the denial notification letter was received

- Closing remarks

Writing an Insurance appeal letter:

Here are the steps to make your insurance appeal letter;

Begin with the basics

Firstly, you have to include all the important details the insurance company that requires to identify your case. Start the letter by specifying your complete name, then include the policy number, and your contact details that include telephone, email, and mailing address.

Next, state the purpose of writing the letter, the situation about which a benefit was denied, the reason mentioned on the notification letter for the denial, and the date when this notification was received. You should also include the name and contact details of the provider.

Include details

When you have presented the apparent facts regarding the case, it’s time to start your argument that why you think your policy covers the expense and the denial be overturned.

A direct reference to the section or sentence in the policy that specifies eligibility for the requested coverage is the first argument to present. You have to be very particular regarding wording. This is because the wording of the policy must correlate the expense description.

Additionally, the following argument is to include a professional opinion upon building that the wording on the policy does indeed support your claim. A doctor or healthcare provider writes this statement that describe why a particular procedure is/was necessary for medical matters. However, the correction should also include in the statement if the provider specified wrongly the service description for which coverage is being requested.

Send your letter

Sending your insurance appeal letter to the insurance company is the final step. Before sending the letter, make a copy of it and all other documents. Select a transmission method on the basis of what the company accepts. Keep proof of successful submission upon sending. Use certified mail in case the letter is sent through the mail and receive the return receipt. When your appeal request has been received in about ten days, you should obtain a confirmation notice.

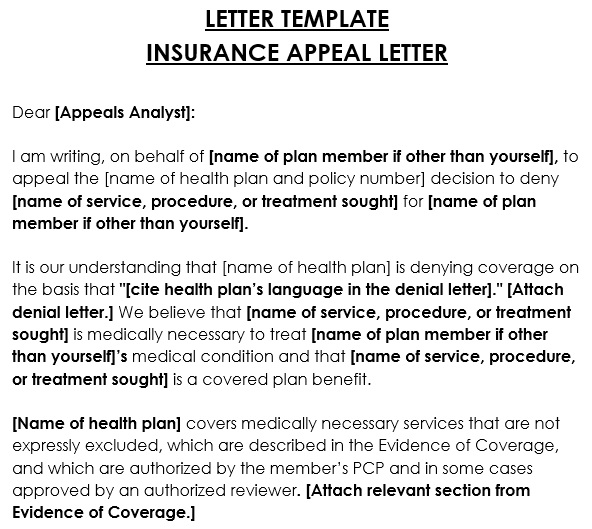

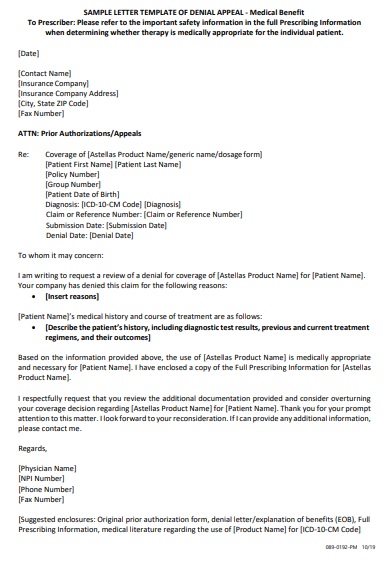

Free Appeal Letter for Denial of an Insurance Claim

Sample Appeal Letter for Denial of an Insurance Claim

Printable Appeal Letter for Denial of an Insurance Claim

Conclusion:

In conclusion, you should present your case by writing an appeal letter for denial of an insurance claim. While writing, you have to be confident about what you are requesting and don’t give up until you get your due.